Expert Insight, Breaking News, and Insider Stories on Real Estate in Paris

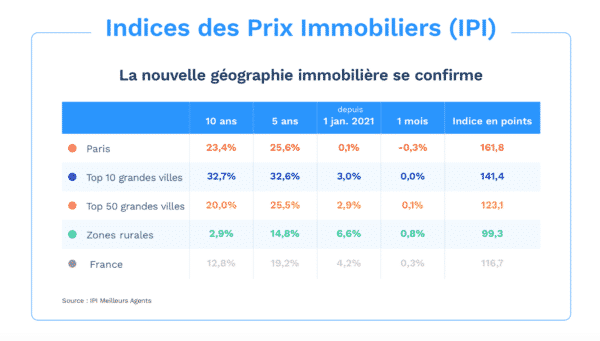

The New Real Estate Geography in France

The disenchantment for big city life, reinforced

The new real estate geography observed by Meilleur Agents. The disenchantment with big cities is marked by an increased interest in the countryside. The hierarchy in terms of price increases until July 2020 was, at the top of the scale, Paris followed by the ten of the largest French cities and, at the bottom, rural areas. Today the standings are reversed. Since the start of 2021, rural areas have thus experienced the strongest growth at the national level (+ 6.6%). That is, more than double the figures recorded by the ten largest metropolises in France during the same time period. And above all … Far ahead of those in the capital (+ 0.1%).

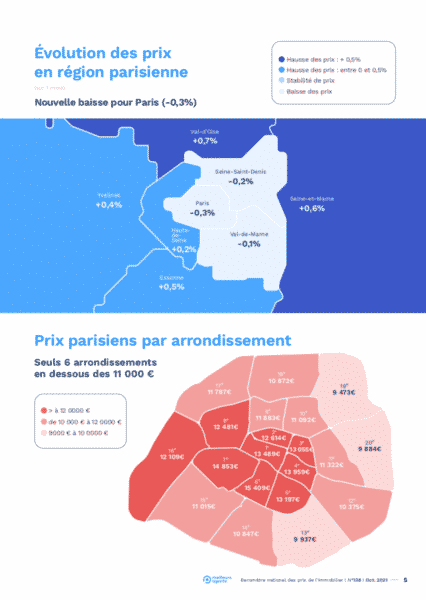

As such, the Paris region alone sums up this paradigm shift. The further away potential buyers move from the city center, the steeper the price increase. In one year, Paris has lost 1.2% while the inner suburbs gained 2.7% and the inner suburbs 5.2%.

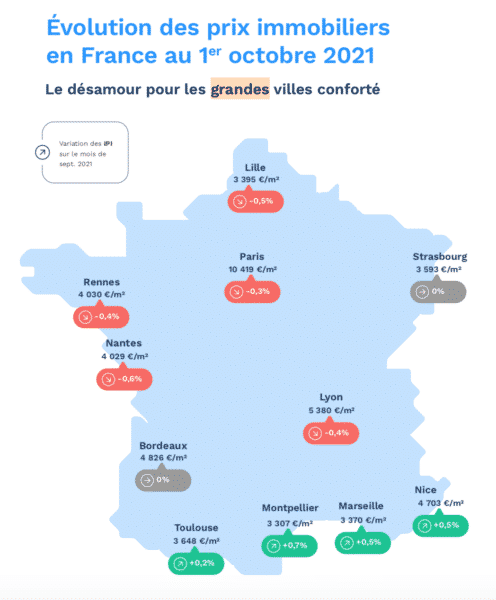

A seasonal release of real estate tension

As every year at the same time, real estate tension eased in September. Far from being worrying, this seasonal drop can be explained by the small number of buyers who start their projects during the summer holidays. This phenomenon affects all major French metropolises without distinction. Thus, the Real Estate Tension Index (ITI) of Meilleur Agents recorded an average decrease of 2 points. Today there are 11% more buyers than sellers in Marseille, Toulouse, Bordeaux and Lille. By comparison, this rate reached 14% in June in the capital of Occitanie. This ratio even fell, with the start of the school year, to 9% in Paris, Nice and Nantes and to 8% in Montpellier and Rennes. As for Lyon, it now has only 5% more buyers than sellers, compared to 10% in June. An almost perfect balance.

It is, however, in Strasbourg that the pool of potential buyers is declining most drastically. In one month, the city saw its ITI go from 16 to 11. If the situation is not surprising in almost all of the eleven largest cities in France, it can however raise questions in the prefecture of the GrandEst region.

More than a simple downturn, we are witnessing a real drop in the number of applicants for property. However, unlike other large agglomerations, this rapid turnaround may raise concerns about a more structural problem. While its counterparts have experienced a phase of gradual stabilization since the start of the health crisis, the Strasbourg market has for its part remained strangely euphoric in terms of both real estate tension and prices. This tightening in demand may be the first signal for a landing there.

No fear on the credit side

The specter of a lasting decline in demand does not seem credible for the experts at Meilleur Agents because rates will remain low and the banks will continue to play their role of financier.

At 1.08% in July (all credit terms combined) according to the Banque de France, the average mortgage rate has reached an all-time low.

And, despite the ambient pessimism, the announcement of the now mandatory nature of what until then was only the recommendations of the High Financial Stability Council (HSCF) on mortgage lending should not change the situation. Why? These measures, which will become binding as of January 1, were in fact already widely applied by banking establishments. As a reminder, the household debt ratio is limited to 35% including insurance, the maximum borrowing period can no longer exceed 25 years (27 years under conditions) and banks are not allowed to withdraw. Excluded from these rules only up to 20% of their volume of new quarterly loans, with particular targeting for purchases of primary residences and first-time buyers.

However, at present, only 20.9% (HCSF report) of the financing files accepted do not meet the standards of the HCSF, that is to say the French credit production is based on sound foundations.

Suffice to say that individuals will always have access to credit without too much difficulty. Not to mention that many “off the nail” files concern rental property investments and purchases of second homes. In other words, buyers who generally have additional savings and who will be able to continue, despite these new constraints, to finance themselves by simply adjusting their personal contribution upwards.

As for the ECB’s latest discussions relating to the slowdown in its asset purchases as part of the PEPP (emergency purchase program in the face of the pandemic), they may make some people fear a shutdown of the credit tap, which should have the effect of stabilizing borrowing rates. Indeed, no announcement of a key rate hike has been made, indicating a status quo that should push banks to continue lending at least in the meantime.

Contact Paris Property Group to learn more about buying or selling property in Paris.